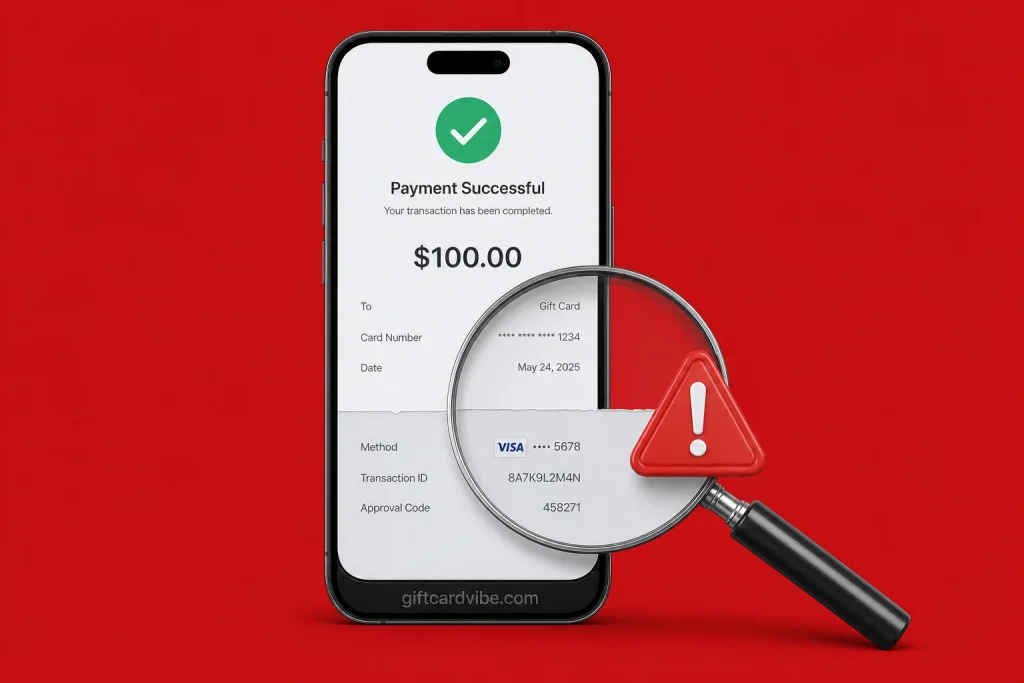

Quick answer: do not release a gift card because a buyer sent a debit alert, transfer receipt, or app screenshot. Open your own bank or wallet through its official app, refresh the transaction history, and confirm that the expected amount is credited and available. A picture can be edited, reused, scheduled, or captured before a transfer fails.

What a screenshot can and cannot prove

| Item shown | What it may indicate | What it cannot establish |

|---|---|---|

| Sender debit alert | The sender’s bank generated a message | That your account received final, available funds |

| Transfer “successful” screen | An instruction was accepted by the sending app | That it settled, was not reversed, or names your real account |

| Reference number | A value formatted like a transaction identifier | That the identifier exists or belongs to this payment |

| Your name on an image | The sender knew the name | That the screenshot came from a banking system |

Verify payment from your side

- Close links and apps opened from the buyer’s message.

- Open your bank or wallet using the app you installed from its official store listing.

- Check the current available balance and transaction ledger, not only SMS or push notifications.

- Match the amount, sender details, date, and reference where your provider displays them.

- If the transaction is pending, unavailable, or absent, treat the order as unpaid.

- Release the card only through the agreed authenticated order flow after credit is confirmed.

Visual warning signs

Edited screenshots often have inconsistent fonts, spacing, number alignment, icon quality, time format, or status labels. Cropped images may hide account details or the app header. But a perfect-looking screenshot is still not proof. Modern editing tools can reproduce an interface accurately, and a genuine screenshot can belong to another transaction.

Do not spend ten minutes doing pixel forensics when a direct ledger check answers the real question.

Common pressure tactics

- “The network is slow; send the code and your alert will arrive.”

- “My account has been debited, so the problem is your bank.”

- “I paid extra; return the difference with another card.”

- “Support will reverse it unless you release the card now.”

- “Here is my ID, so you can trust the screenshot.”

A photo of an ID can be stolen and urgency is not settlement. Pause the trade. A genuine buyer can wait for verifiable payment or use a platform with an escrowed, traceable process.

If the buyer claims a failed or delayed transfer

Ask the sender to resolve it with the sending institution. Do not call a number supplied in the screenshot. Use your own provider’s official support route and give only the transfer reference and non-sensitive account information requested. Do not share OTPs, PINs, passwords, screen-sharing access, or remote-control access.

If you already released the gift card

- Contact the gift card issuer immediately and ask whether the value can be frozen.

- Preserve the card, receipt, chat export, phone number, profile URL, screenshot, and timestamps.

- Report the receiving account to your bank or wallet provider through its fraud channel.

- Report the profile on the messaging or social platform.

- For a Nigerian consumer complaint, review the FCCPC documentation process.

The FTC gift card scam guide also advises reporting to the card issuer quickly and keeping the card and store receipt. Recovery is not guaranteed, but speed and complete evidence matter.

A better trade workflow

Use a platform or business account that creates an order before sensitive details are exchanged. The order should state the card, quote, review conditions, payment destination, and dispute route. Compare platform controls on The Legit List and read the latest Scam Radar guides. Neither page replaces checking your own settled balance.

Payment screenshot FAQ

Is a bank debit alert proof that I was paid?

No. It describes the sender’s side and may be fake or unrelated. Confirm the credit in your own account ledger.

What if my SMS alert is delayed?

Use the official bank or wallet app and check available balance and transactions. If credit is absent, do not release the card.

Can a real transfer be reversed?

Payment systems and account types have different dispute and reversal rules. Confirm settled funds and keep a complete order record rather than relying on a screenshot.

Should I call the bank number shown on the receipt?

No. Find the official contact independently from your bank’s app, card, or website.